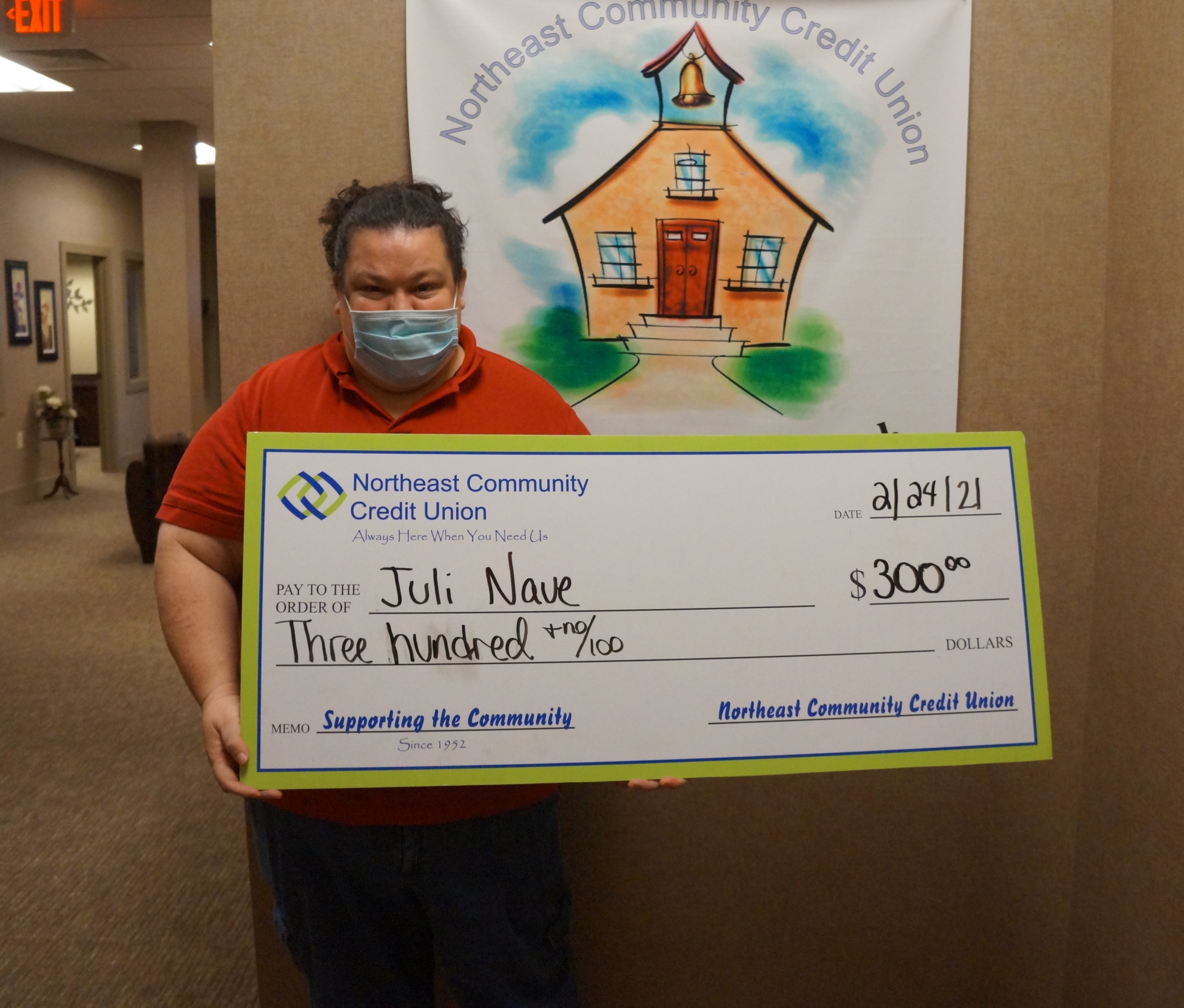

Juli Nave, director of the Family Resource Center for Carter County Schools, is the latest Northeast Community Credit Union Helping Teacher’s Teach grant winner.

Nave plans to use the grant to start a mini food pantry for Carter County School students. The pantry will be stocked with items like granola bars, cereals, rice, beans, peanut butter, bread, coffee, tea and macaroni and cheese. The funding could also be used to help supplement existing food pantries at individual schools.

“The Covid pandemic is still happening,” Nave said. “Some parents have lost jobs, so food may be hard to come by for some families. Having access to extra food would be a blessing to some of our students.”

Northeast Community Credit Union awards $300 every month to a classroom to be utilized for classroom needs, classroom activities, and academic enrichment. Helping Teachers Teach is open to teachers within Carter, Johnson, Unicoi, Sullivan and Washington counties who are members of Northeast Community Credit Union. Area teachers may become members online or at any NCCU location and can download the grant application on the credit union’s website: www.BeMyCU.org.

(ARM) as part of their annual partnership with the non-profit agency.

(ARM) as part of their annual partnership with the non-profit agency. Animal Shelter in their community sponsorship efforts. NCCU recently presented a $500 donation as part of the annual partnership to ECCAS Director Shannon Posada.

Animal Shelter in their community sponsorship efforts. NCCU recently presented a $500 donation as part of the annual partnership to ECCAS Director Shannon Posada.

$1,000 to the Carter County Imagination Library.

$1,000 to the Carter County Imagination Library.

Home and Academy to help them continue their goal of “Growing Girls God’s Way.”

Home and Academy to help them continue their goal of “Growing Girls God’s Way.”

community sponsorship efforts. NCCU recently presented a donation as part of its annual partnership to Recovery Soldiers Ministries Program Director EJ Eggers.

community sponsorship efforts. NCCU recently presented a donation as part of its annual partnership to Recovery Soldiers Ministries Program Director EJ Eggers.

Chamber of Commerce Chamber Youth Ambassador Program.

Chamber of Commerce Chamber Youth Ambassador Program.