Northeast Community Credit Union presented a $500 donation to the United Way of  Elizabethton/Carter County and Johnson County as part of their annual partnership with the non-profit agency.

Elizabethton/Carter County and Johnson County as part of their annual partnership with the non-profit agency.

The United Way relies on community donations to provide assistance to thousands of individuals through partnerships with other non-profit community organizations.

These partnerships include Boys and Girls Club of Elizabethton/Carter County, Assistance and Resources Ministries, Elizabethton Senior Citizens Center, 211 Contact Ministries, Adult Day Services, American Red Cross, Elizabethton Neighborhood Service Center, Personal Support Services, and the Boy Scouts Sequoyah Council.

United Way Director Crystal Carter said it was community efforts that kept the United Way campaign on track. NCCU’s donation will be used to help fund literacy projects sponsored by the Boys and Girls Club of Elizabethton/Carter County in the United Way of Elizabethton/Carter County and Johnson County service area.

To donate to United Way or for more information, call 423-543-6975 or email, director@uwayecc.org

Northeast Community Credit Union has been serving the community since October 1952 when it was chartered as a credit union by the State of Tennessee. Northeast Community Credit Union is a not-for-profit financial cooperative. It is open to anyone who lives, works, worships or attends school in Carter, Johnson, Washington, Unicoi and Sullivan counties along with their immediate family members.

Animal Shelter in their community sponsorship efforts. NCCU Electronic Services Manager Regina Chambers recently presented a $500 donation as part of the annual partnership to ECCAS Director Shannon Posada.

Animal Shelter in their community sponsorship efforts. NCCU Electronic Services Manager Regina Chambers recently presented a $500 donation as part of the annual partnership to ECCAS Director Shannon Posada. Credit Union Helping Teacher’s Teach winner.

Credit Union Helping Teacher’s Teach winner. community sponsorship efforts. NCCU Community Engagement Director Kathy Campbell recently presented a $500 donation as part of the annual partnership to Recovery Soldiers Ministries Program Director Ben Cole.

community sponsorship efforts. NCCU Community Engagement Director Kathy Campbell recently presented a $500 donation as part of the annual partnership to Recovery Soldiers Ministries Program Director Ben Cole.

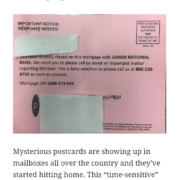

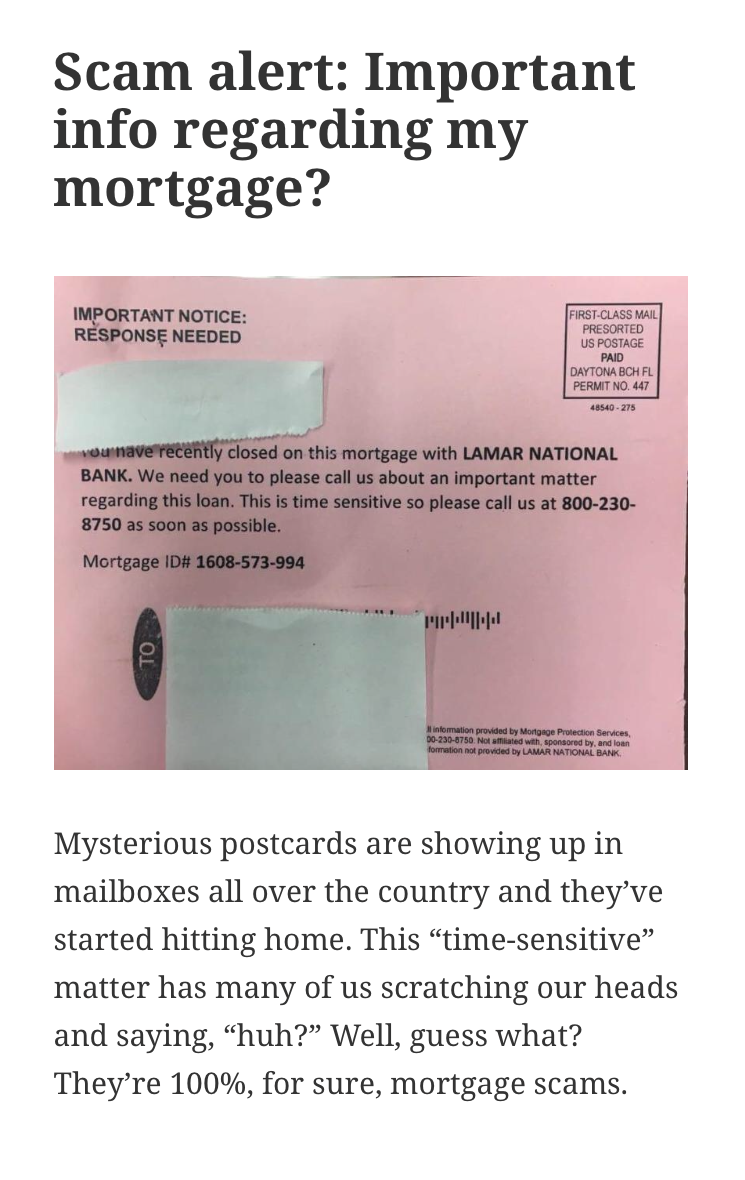

information on your mortgage. These are a scam. If you receive one of these postcards, you do not need to call the 1-800 number on the card and you do not need to take any further action. Simply throw the card away.

information on your mortgage. These are a scam. If you receive one of these postcards, you do not need to call the 1-800 number on the card and you do not need to take any further action. Simply throw the card away.

Center’s Magic Movement Program.

Center’s Magic Movement Program.

Elizabethton.

Elizabethton.