Matt Wilson, English teacher and Speech and Debate coach at Happy Valley High School, is the latest![]() Northeast Community Credit Union Helping Teachers Teach grant winner.

Northeast Community Credit Union Helping Teachers Teach grant winner.

The Happy Valley High Speech & Debate Team will be participating in the National Speech and Debate Association National Tournament in June. The HTT grant will help pay for the students’ entry fees and travel costs to the competitions.

“This affords the team members the opportunity to compete in public speaking events,” Wilson said. “Competing against students from around the country and doing so on the campus of the University of Richmond will expand my students’ horizons and make their worlds a little larger.”

Northeast Community Credit Union awards $300 every month to a classroom to be utilized for classroom needs, classroom activities, and academic enrichment. Helping Teachers Teach is open to teachers within Carter, Johnson, Unicoi, Sullivan and Washington counties who are members of Northeast Community Credit Union. Area teachers may become members online or at any NCCU location and can download the grant application on the credit union’s website: www.BeMyCU.org.

Alex Campbell, social studies teacher at Elizabethton High School, is the latest Northeast Community Credit Union Helping Teachers Teach grant winner.

Credit Union Helping Teachers Teach grant winner.

Campbell applied for the grant to help cover the cost of publishing 500 copies of a book his sociology class has been working on. Students have been writing a research-based book about nine active, or potentially active, serial killers in Tennessee in the 1980s. Students focused on ethical research practices, responsible storytelling and careful documentation.

“My students work on real cold cases, focusing on making a real impact,” Campbell said. “The ability for students to see their work have actual impact in helping people across our state, and many others, is invaluable. What this money will help us do is get this information out to help law enforcement make connections between cases, show how certain confirmed murderers should be considered suspects in many cases, and reignite public interest to help draw attention to these cases.”

Jan Carol Publishing plans to launch “Driven by Rage Fueled by Diesel – The Forgotten Victims of the Tennessee Highway Hunters” by Elizabethton High School Tennessee Student Investigators in May with a nationwide media campaign.

Northeast Community Credit Union awards $300 every month to a classroom to be utilized for classroom needs, classroom activities, and academic enrichment. Helping Teachers Teach is open to teachers within Carter, Johnson, Unicoi, Sullivan and Washington counties who are members of Northeast Community Credit Union. Area teachers may become members online or at any NCCU location and can download the grant application on the credit union’s website: www.BeMyCU.org.

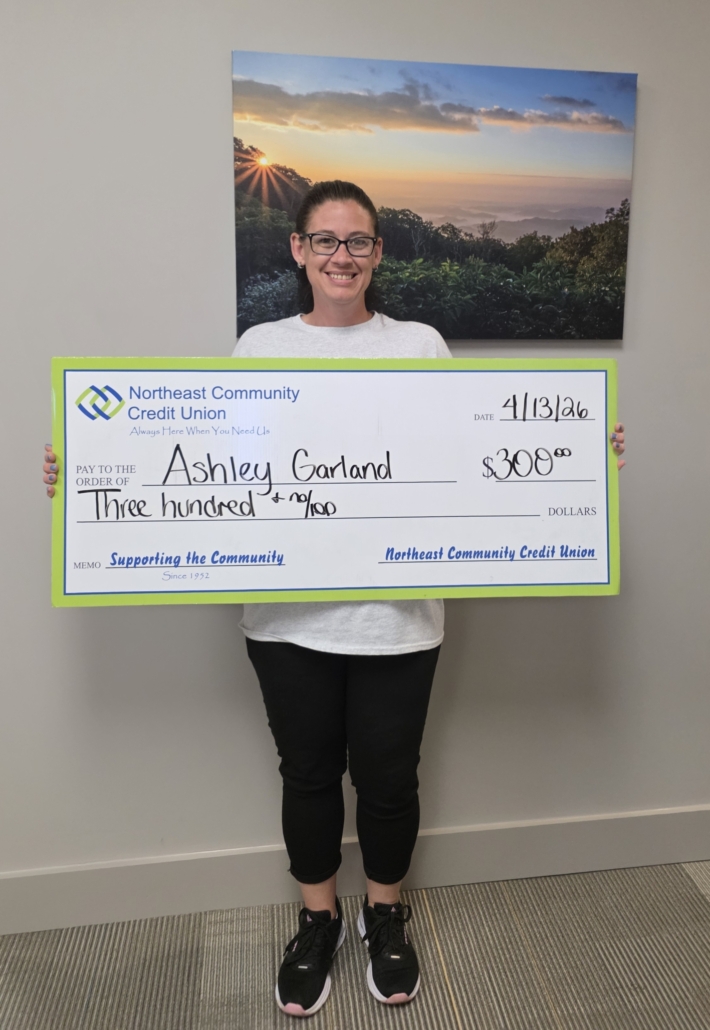

Ashley Garland, special education aide at Unaka High School, is the latest Northeast Community Credit Union Helping Teachers Teach grant winner.

Union Helping Teachers Teach grant winner.

Garland applied for the grant to help cover the cost of the CDC class Student-Run Coffee Cart. Students gain real-world experience in business management, finance and marketing by taking orders, counting money, delivering drinks, and tracking order data.

“This project offers a hands-on learning experience,” Garland said. “It also helps with social skills and life skills.”

Northeast Community Credit Union awards $300 every month to a classroom to be utilized for classroom needs, classroom activities, and academic enrichment. Helping Teachers Teach is open to teachers within Carter, Johnson, Unicoi, Sullivan and Washington counties who are members of Northeast Community Credit Union. Area teachers may become members online or at any NCCU location and can download the grant application on the credit union’s website: www.BeMyCU.org.

Alisa Buckner, librarian at Cloudland Elementary School, is the latest Northeast Community Credit Union Helping Teachers Teach grant winner.

Buckner applied for the grant to help cover the cost to buy new books for the school’s library. She said the current library collection is challenged with aging, worn materials that have been heavily used along with outdated items that are no longer relevant to students.

“A well-stocked library is essential for meeting the academic, social and emotional needs of today’s learners,” Buckner said. “New books provide students with high-interest, age-appropriate reading materials that reflect their lives, cultures and interests. When students see themselves represented in books and are exposed to perspectives different from their own, they are likely to engage deeply with reading.”

Northeast Community Credit Union awards $300 every month to a classroom to be utilized for classroom needs, classroom activities, and academic enrichment. Helping Teachers Teach is open to teachers within Carter, Johnson, Unicoi, Sullivan and Washington counties who are members of Northeast Community Credit Union. Area teachers may become members online or at any NCCU location and can download the grant application on the credit union’s website: www.BeMyCU.org.

Jessica Hayes, science teacher at Elizabethton High School, is the latest Northeast Community Credit

Union Helping Teachers Teach grant winner.

Hayes applied for the grant to help cover the cost of buzzer lockout system for the EHS Science Bowl team. The system will allow the team to practice under the same conditions they will experience at the actual event. When not being used by the team, science classes at EHS will use the buzzer system to study for exams. Any remaining funding will be used to purchase gas and supplies for the team’s trip to compete at the Oak Ridge National Laboratories Science Bowl.

“We compete against a lot of well to do schools at the competition,” Hayes said. “These funds will help us to prepare and even the playing field against these schools that seem to have unlimited funding. The Elizabethton community is very near and dear to my heart. I believe in our students. They can compete at high levels and I want them to have the same opportunities to compete at those high standards as other schools.”

Northeast Community Credit Union awards $300 every month to a classroom to be utilized for classroom needs, classroom activities, and academic enrichment. Helping Teachers Teach is open to teachers within Carter, Johnson, Unicoi, Sullivan and Washington counties who are members of Northeast Community Credit Union. Area teachers may become members online or at any NCCU location and can download the grant application on the credit union’s website: www.BeMyCU.org.