Northeast Community Credit Union is investing in the children of Carter County with a donation of $1,000 to the Carter County Imagination Library.

$1,000 to the Carter County Imagination Library.

Northeast Community Credit Union is a Foundation Member of CCIL and has contributed thousands of dollars since the start of Carter County Imagination Library. Carter County Imagination Library provides a free book to children in Carter County every month from birth until they turn five years old.

According to the CCIL, more than 2,200 books are distributed monthly to children in Carter County and Elizabethton, representing 91.43% enrollment. Community contributions help cover the $2,500 monthly cost not covered by the state.

Presenting this year’s donation on behalf of NCCU to Carter County Imagination Library Chair Summer Johnson (left) is Elizabeth Bradley, New Accounts Representative.

To donate to the Imagination Library, contact the Elizabethton/Carter County Public Library at (423) 547-6360.

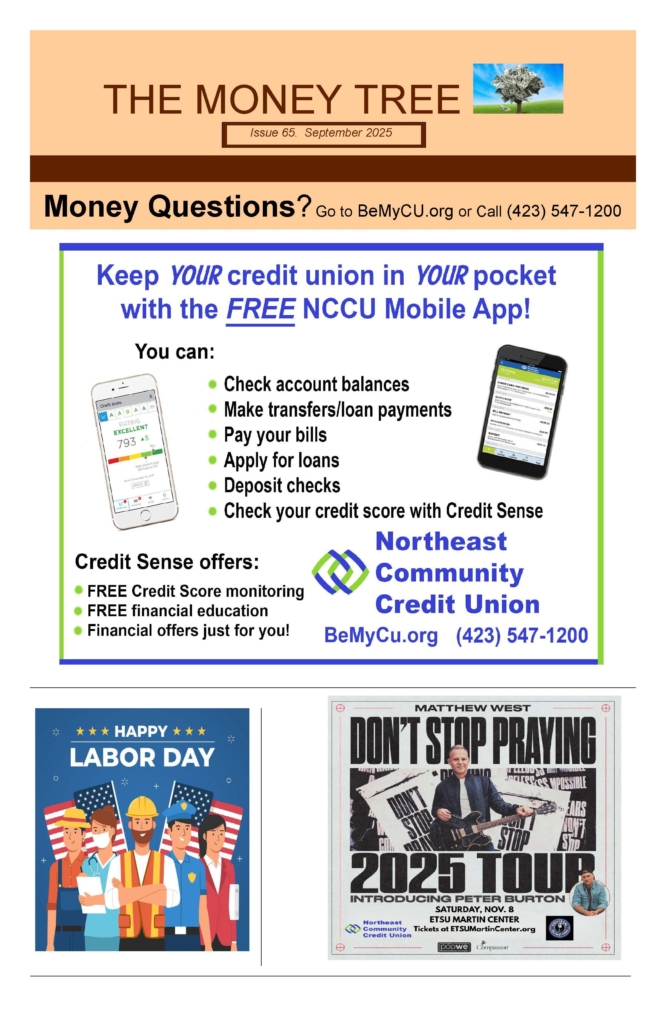

Northeast Community Credit Union is a major contributor in the local community and has been providing service since October 1952 when it was chartered as a credit union by the State of Tennessee. Northeast Community Credit Union is a not-for-profit financial cooperative focused on youth financial education, providing convenient low-cost financial products and service to help families have richer futures, and growing strong local businesses while serving anyone who lives, works, worships or attends school in Carter, Johnson, Washington, Unicoi and Sullivan counties along with their family members.

Community Credit Union Helping Teachers Teach grant winner.

Community Credit Union Helping Teachers Teach grant winner.

Credit Union Helping Teachers Teach grant winner.

Credit Union Helping Teachers Teach grant winner. by sponsoring both of Carter County’s backpack programs.

by sponsoring both of Carter County’s backpack programs.