Northeast Community Credit Union is honored to announce it has once again earned BauerFinancial’s highest 5-Star Superior rating.

highest 5-Star Superior rating.

A 5-Star rating indicates that Northeast Community Credit Union is one of the strongest financial institutions in the nation, excelling in such areas as capital, loan quality, profitability and much more.

Bauer Financial is the nation’s leading independent bank and credit union rating and research firm since 1983. The 5-Star rating is the highest ranking the banking industry research firm can assign a financial institution and denotes the highest level of financial performance.

NCCU has also earned the placement of being on Bauer Financials “Recommended Credit Union Report.”

“The 5-Star Rating by BauerFinancial indicates that Northeast Community Credit Union excels in nearly all measurable areas,” said NCCU President/CEO Teresa Arnold. “The rating places us in the top tier of financial institutions in the United States. We are honored by the ranking and are committed to continue providing the highest level of service to our members every day. The credit union has maintained its top-tier status for decades. What this means for this community is that our institution is safe, financially sound, and consistently operating well above all regulatory capital requirements.”

Northeast Community Credit Union has been serving the community since October 1952 when it was chartered as a credit union by the State of Tennessee. Northeast Community Credit Union is a not-for-profit financial cooperative. It is open to anyone who lives, works, worships or attends school in Carter, Johnson, Washington, Unicoi and Sullivan counties along with their immediate family members.

For more information, visit www.BeMyCU.org or call 423-547-1200.

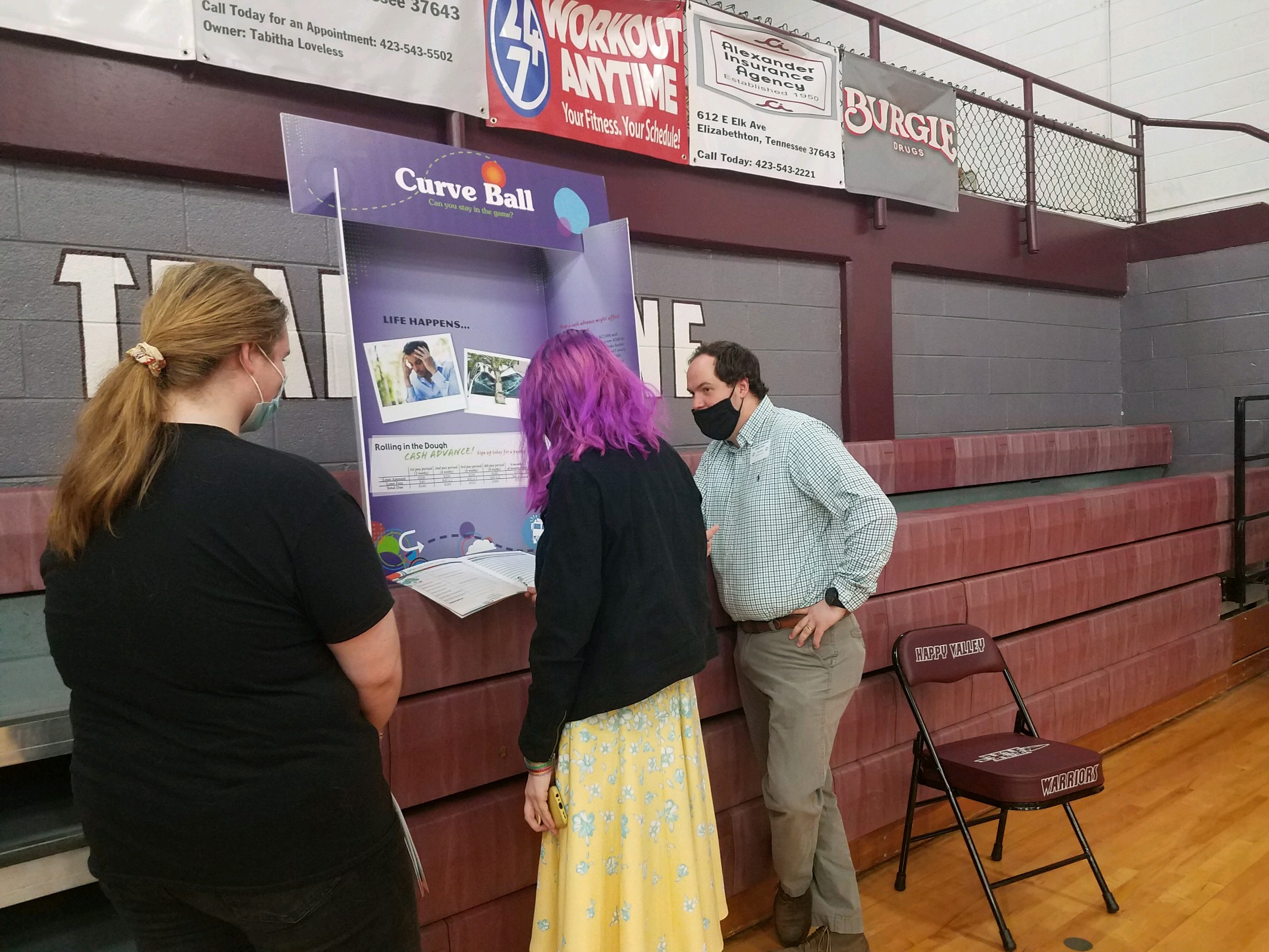

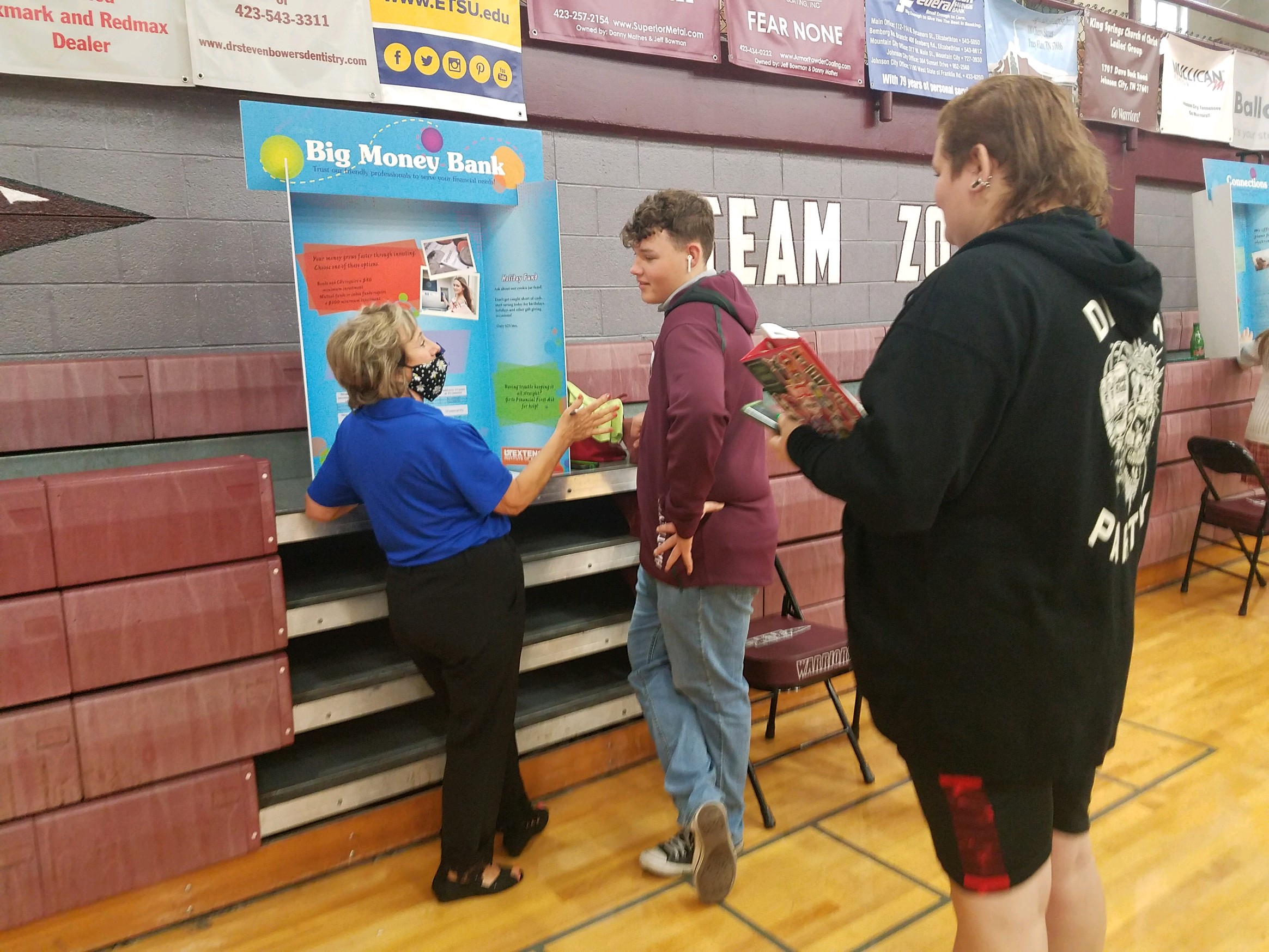

This ‘Real Life’ Simulation includes coaching teens through choosing careers, buying cars, finding homes, and how to handle those annoying ’curveballs’ life throws at us.

This ‘Real Life’ Simulation includes coaching teens through choosing careers, buying cars, finding homes, and how to handle those annoying ’curveballs’ life throws at us.

Year Celebration event to reward the students for all their hard

Year Celebration event to reward the students for all their hard work during this unconventional school year.

work during this unconventional school year. Winegar, second-grade teacher at Happy Valley Elementary. “We want to celebrate their efforts and success as we wrap up the 2020-2021 school year.”

Winegar, second-grade teacher at Happy Valley Elementary. “We want to celebrate their efforts and success as we wrap up the 2020-2021 school year.” union by the State of Tennessee. Northeast Community Credit Union is a not-for-profit financial cooperative. It is open to anyone who lives, works, worships or attends school in Carter, Johnson, Washington, Unicoi and Sullivan counties along with their immediate family

union by the State of Tennessee. Northeast Community Credit Union is a not-for-profit financial cooperative. It is open to anyone who lives, works, worships or attends school in Carter, Johnson, Washington, Unicoi and Sullivan counties along with their immediate family  members.

members. Credit Union Helping Teacher’s Teach grant winner.

Credit Union Helping Teacher’s Teach grant winner. Malone plans to use the grant to purchase two Polaroid instant cameras and film. This equipment would allow Malone’s students to create a “math newsletter” along with other projects such as a monthly classroom bulletin board, lesson projects and presentation boards.

Malone plans to use the grant to purchase two Polaroid instant cameras and film. This equipment would allow Malone’s students to create a “math newsletter” along with other projects such as a monthly classroom bulletin board, lesson projects and presentation boards. the school to see.”

the school to see.” Northeast Community Credit Union awards $300 every month to a classroom to be utilized for classroom needs, classroom activities, and academic enrichment. Helping Teachers Teach is open to teachers within Carter, Johnson, Unicoi, Sullivan and Washington counties who are members of Northeast Community Credit Union. Area teachers may become members online or at any NCCU location and can download the grant application on the credit union’s website: www.BeMyCU.org.

Northeast Community Credit Union awards $300 every month to a classroom to be utilized for classroom needs, classroom activities, and academic enrichment. Helping Teachers Teach is open to teachers within Carter, Johnson, Unicoi, Sullivan and Washington counties who are members of Northeast Community Credit Union. Area teachers may become members online or at any NCCU location and can download the grant application on the credit union’s website: www.BeMyCU.org.

AdaptoPlay serves children with disabilities from spinal cord injuries, traumatic brain injuries, strokes, cerebral palsy, amputations, muscular dystrophy, neuromuscular disease, deafness/hearing impairments, blindness/vision impairment and others.

AdaptoPlay serves children with disabilities from spinal cord injuries, traumatic brain injuries, strokes, cerebral palsy, amputations, muscular dystrophy, neuromuscular disease, deafness/hearing impairments, blindness/vision impairment and others.

“We have witnessed firsthand how hard the students have worked during virtual learning and how they are doing everything they can to stay in face-to-face learning,” Sadie Fletcher, faculty at Doe Elementary, said. “Students are taking extra precautions and going the extra mile to keep themselves and their classmates safe and healthy. They have made it through an entire school year of new procedures and policies and we at Doe feel like they deserve to be celebrated for those accomplishments.”

“We have witnessed firsthand how hard the students have worked during virtual learning and how they are doing everything they can to stay in face-to-face learning,” Sadie Fletcher, faculty at Doe Elementary, said. “Students are taking extra precautions and going the extra mile to keep themselves and their classmates safe and healthy. They have made it through an entire school year of new procedures and policies and we at Doe feel like they deserve to be celebrated for those accomplishments.”